Before You Retire

- Get ride of your debt.

- Don't enter into a car loan before entering into retirement. Pay cash for cars.

- Evaluate your insurance. Maybe you don't your life insurance, etc.

- Determine how you are going to pay for healthcare. Most Canadians pay these extra expenses out of pocket.

- Update your estate plan (will, power of attorney, document your digital assets(logins, etc).

- Determine your retirement age. (Will need to line up with your retirement plan!)

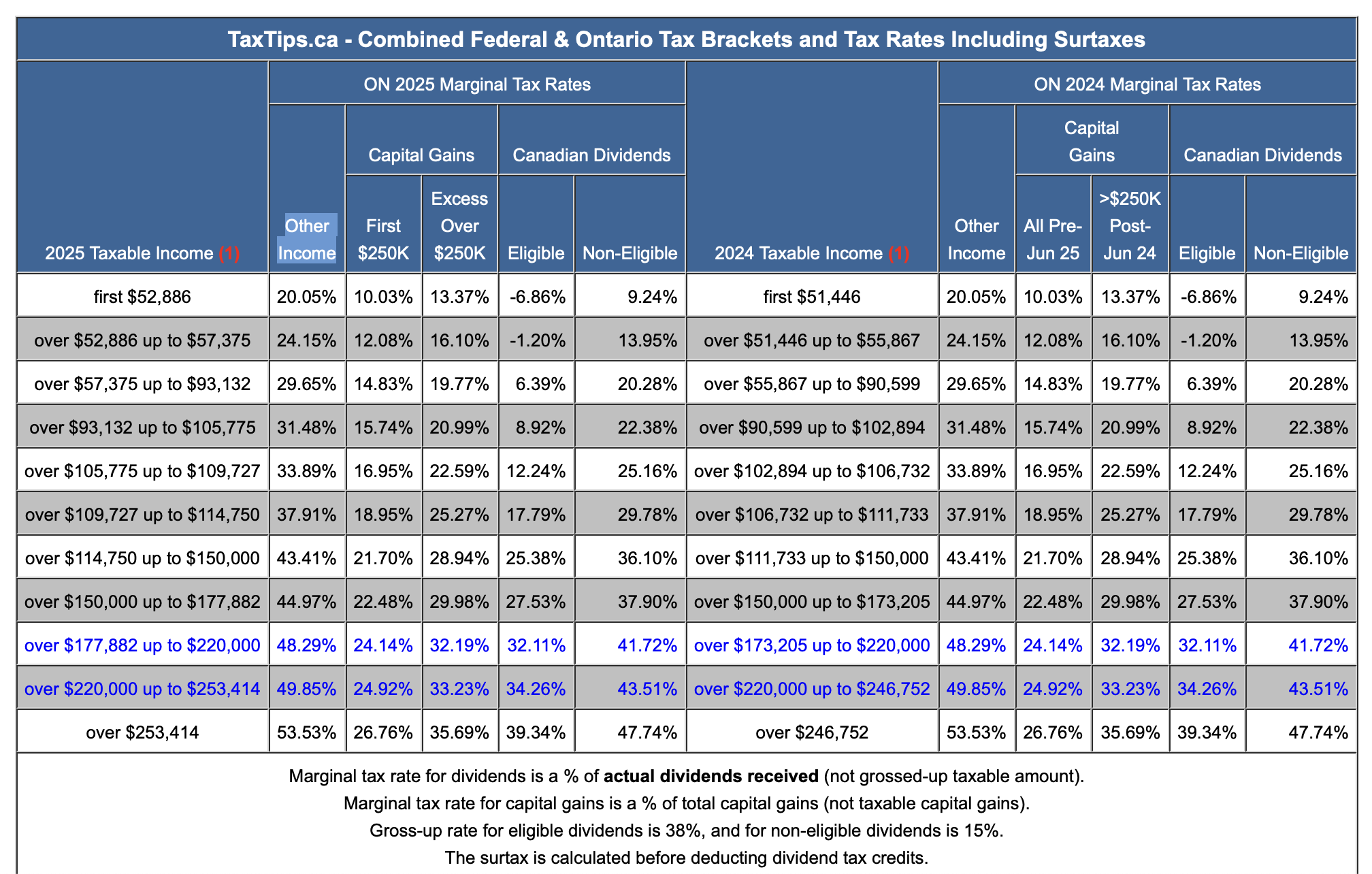

Tax Rates

Retirement Budget

Figure out how much you need monthly once you retired.

Having money in a TFSA will help if you have a big expense, bucket list item, etc... since they don't count as income.

Income Base on Savings

Assumptions:

- Retiring at 60

- CPP at age 70, 75% of max

- Running estate to $0 until

- From age 60 to 95

| Total Savings | 500k | 750k | 1 mil |

|---|---|---|---|

| RRSP Savings | 400k | 550k | 800k |

| TFSA Savings | 100k | 200k | 200k |

Couple Yearly Income After Tax (Adjusted for Inflation) | $57,365 | $66,480 | $74,757 |

Single Yearly Income After Tax (Adjusted for Inflation) | $37,376 | $45,290 | $53,042 |

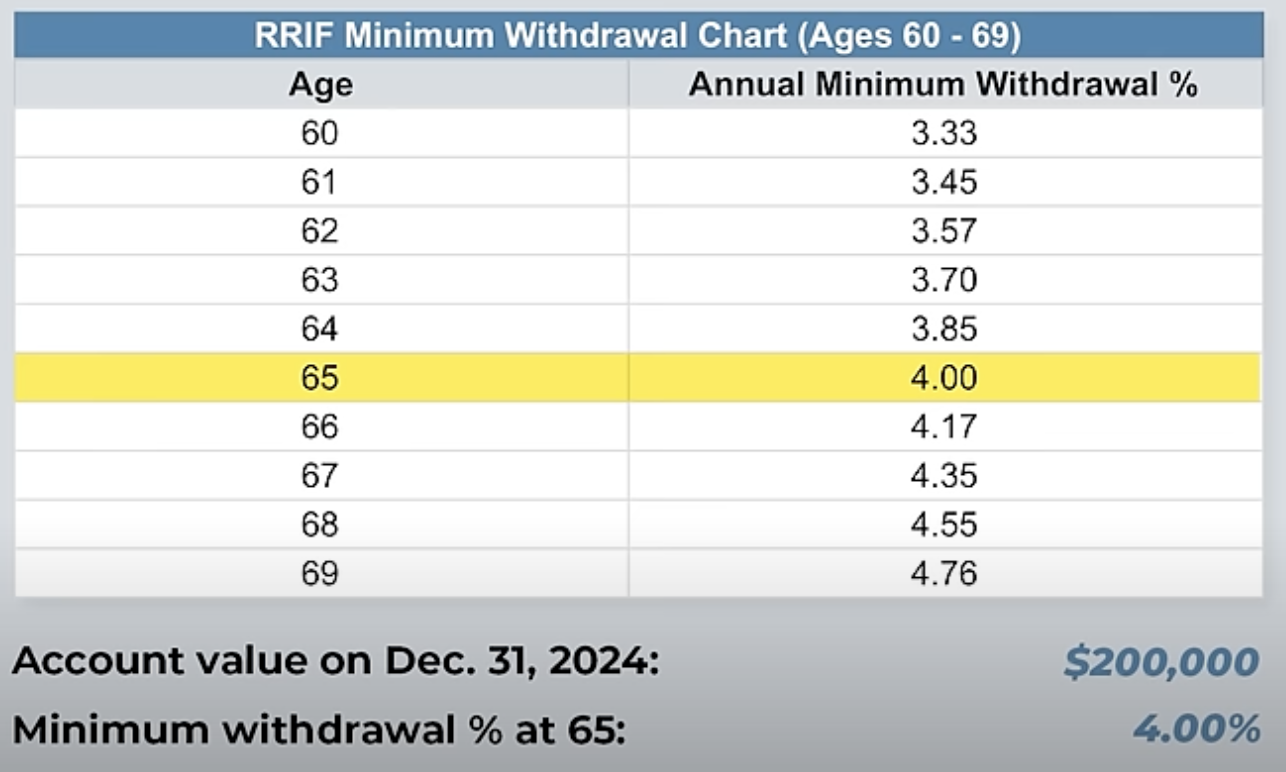

RRIF

Earnings in a RRIF are tax-free and amounts paid out of a RRIF are taxable on receipt.

When you retire, your RRSP needs to be converted to a RRIF before the age of 71.

At 71, you will be forced to convert your RRSP to a RRIF.

At 72, you need to start withdrawing from it.

There is a minimum amount that you need to withdraw once converted to a RRIF.

It is very unlikely that you would ever just take out the minimum.

Benefits of a RRIF over RRSP

- no commissions on withdrawal

- income splitting if 65 or older

- no withholding tax on the minimum, there is a withholding tax above the minimum.

Withholding Rates

- 10% on amounts up to $5,000

- 20% on amounts over to $5,000

- 30% on amounts up to $15,000

RRSP Meltdown Strategy

The RRSP Meltdown Strategy is an aggressive drawdown of your RRSP(RRIF) early in retirement.

- Drawing down your RRSP will allow you to delay your CPP/OAC.

- Money left in your RRSP(RRIF) upon your death will be taxed as if it was income received in that one year.

- You can use your TFSA for emergencies while pulling an income from your RRSP(RRIF). ie. new roof, etc...

TFSA

- Use it as a lever account. If you need some extra money, pull it from your TFSA account.

- Over contributing to your TFSA are subject to a 1% penalty tax per month charged on the excess amount.

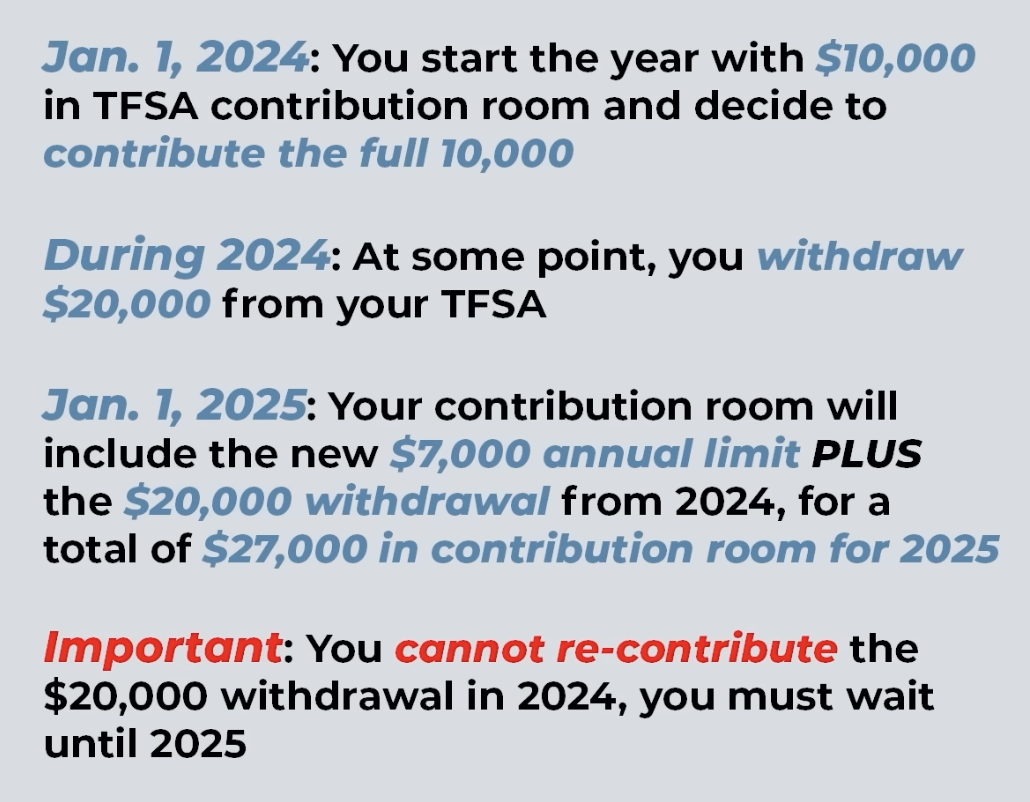

Withdrawal Example

Moving Abroad

- You can keep your TFSA

- As a non-resident, you won't accumulate new contribution room and you won't be able to contribute to your TFSA

References

| Reference | URL |

|---|---|

| 20 Years of Canadian Retirement Knowledge In 1hr 57mins | https://www.youtube.com/watch?v=r9Da-mb-zSw&t=1667s |

| Budget Tracker and Net Worth Tracker | https://www.parallelwealth.com/tools |